What would you need to earn to own a home in San Jose or Pittsburgh?

The answer might surprise you. With the housing market fluctuations and diverse economic landscapes, knowing the salary needed to buy a home in U.S. cities is crucial for making informed decisions.

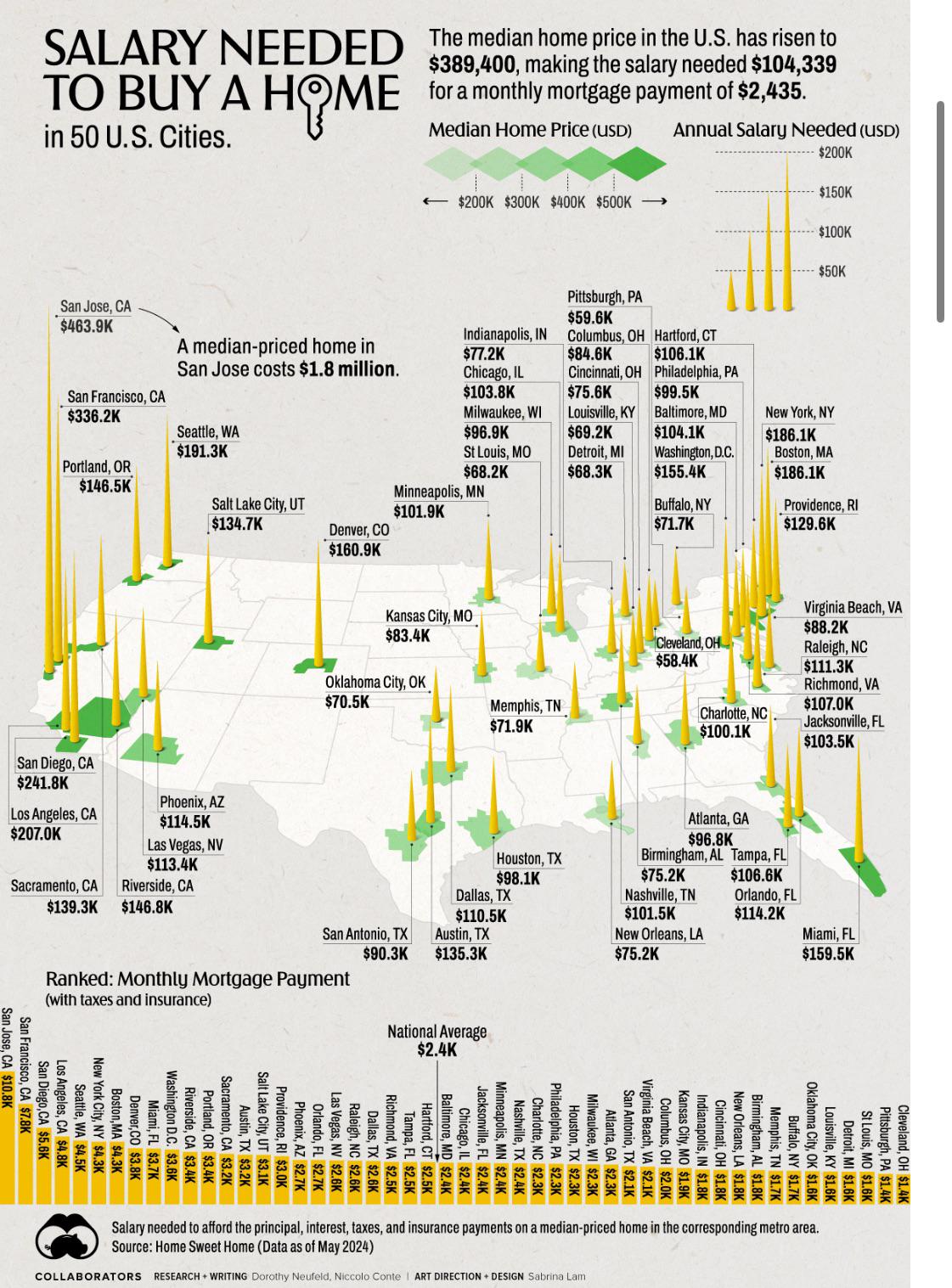

This article dives into the latest data, highlighting stark differences in income requirements across America's largest metropolitan areas. You'll discover surprising findings, such as needing an annual salary of $454,296 in San Jose, CA, compared to just $58,232 in Pittsburgh, PA.

Understanding these income requirements can shape your home-buying strategy and financial planning—as we explore in detail.

Understanding the Salary Needed to Buy a Home in U.S. Cities

Grasping the income requirements for home buying is essential for prospective homeowners seeking to navigate the housing market effectively. With economic fluctuations and varying property values, knowing the salary needed to buy a home in U.S. cities provides a realistic picture of affordability. The study updated on February 12, 2025, offers insights into the salary required to afford a median-priced home in the 50 largest metropolitan areas in the U.S., helping buyers align their financial planning with current market conditions.

- San Jose, CA: $454,296

- San Francisco, CA: $336,200

- Seattle, WA: $191,300

- Denver, CO: $160,900

- Pittsburgh, PA: $58,232

The significance of this data lies in its ability to inform potential buyers about the annual income for mortgage approval across different cities. By comparing salary needs, individuals can make informed decisions about where to settle based on their financial capabilities and lifestyle preferences. This data is pivotal in understanding regional disparities and ensuring that financial commitments align with personal budgets.

Comparing Home Affordability Across U.S. Cities

Home affordability varies significantly across U.S. cities due to several influencing factors. Median home prices are a primary determinant, directly impacting the salary required to purchase a property. Additionally, property taxes and HOA fees can vary widely, adding to the overall cost of homeownership. Insurance costs are another consideration that can differ based on location-specific risks such as natural disasters. The cost of living in a city, including everyday expenses like groceries and utilities, further affects affordability. For example, while Honolulu is 30% cheaper than San Francisco in terms of housing, the disparity in salaries, which are 40% to 60% lower in Honolulu, underscores the complexity of affordability assessments.

| City | Median Home Price | Required Salary |

|—————-|——————-|—————–|

| San Jose, CA | $1,500,000 | $454,296 |

| San Francisco, CA | $1,300,000 | $336,200 |

| Seattle, WA | $900,000 | $191,300 |

| Denver, CO | $750,000 | $160,900 |

| Pittsburgh, PA | $250,000 | $58,232 |

The disparities illustrated in the table highlight the importance of considering multiple factors when evaluating home affordability. While cities like San Jose and San Francisco require high salaries due to elevated home prices, locations such as Pittsburgh offer more affordable options. However, even in cities with lower home prices, the overall cost of living and available income levels must be considered to ensure a comprehensive understanding of affordability. These comparisons aid potential buyers in making informed decisions about where to settle, aligning their financial strategies with regional economic realities.

The Impact of Mortgage Rates and Property Taxes

Mortgage rates play a crucial role in determining the monthly payments and the overall financial prerequisites for buying a home. Lower mortgage rates reduce monthly payments, thereby decreasing the salary needed to buy a home. Conversely, higher rates can significantly increase these payments, making homeownership less affordable for many. The study provides resources such as current mortgage rates and state-specific lender information, allowing potential buyers to calculate their expected payments accurately. Utilizing these tools and guides for mortgage calculations can aid in aligning one's salary with feasible homebuying options.

Property taxes also have a substantial impact on home affordability. These taxes vary greatly by state and locality, affecting the total cost of homeownership. In areas with high property taxes, the required salary to maintain a home increases, as these taxes add to the recurring expenses homeowners must manage. Tax considerations for homeowners are essential when evaluating the affordability of a particular area, as they can alter the perceived cost-effectiveness of purchasing a home in regions with otherwise favorable conditions.

Overall, both mortgage rates and property taxes are significant factors that influence the salary required for homeownership. They shape the economic landscape of homebuying by affecting monthly payments and long-term financial commitments. Understanding these elements is vital for potential buyers, as they contribute to the complexity of making informed decisions about where and when to purchase a home. By considering these variables, individuals can better prepare themselves financially, ensuring that their homebuying decisions align with their economic realities.

Exploring Financial Strategies for Homebuyers

Saving for a down payment is a critical step in the journey to homeownership. How much should one save for a down payment? Typically, a down payment ranges from 3% to 20% of the home's purchase price. Saving a larger down payment can reduce the loan amount, lower monthly payments, and potentially eliminate the need for private mortgage insurance (PMI). First-time homebuyers can benefit from guides and reviews of mortgage lenders to find favorable terms and understand the financial landscape. Establishing a dedicated savings plan and sticking to it is essential for accumulating the necessary funds.

- Create a budget and stick to it.

- Research and compare mortgage lenders.

- Explore refinancing options.

- Consider home equity and investment opportunities.

- Utilize financial planning tools and resources.

Financial planning plays a pivotal role in achieving homeownership. Why is financial planning important for buying a home? It allows individuals to assess their financial health, set realistic goals, and manage their resources effectively. Comprehensive planning involves evaluating home equity options and exploring refinancing opportunities to optimize financial commitments. Investing in private growth companies through platforms like Fundrise Venture can also be a strategic move to increase savings. By leveraging financial planning tools, potential homebuyers can navigate the complexities of the housing market and make informed decisions that align with their long-term goals.

Evaluating Urban vs. Suburban Housing Costs

Urban housing expenses are typically higher due to the demand for proximity to job opportunities, cultural amenities, and infrastructure. What are the potential benefits of living in expensive cities? Higher income opportunities often offset these costs, making it strategic for wealth building. Urban areas offer diverse employment options, potentially leading to career advancement and salary growth. Additionally, access to public transportation can reduce commuting costs, providing further financial balance.

In contrast, suburban housing costs are generally lower, offering more space for less money. How do suburban housing costs compare to urban expenses? Suburban areas provide larger homes and yards at more affordable prices, appealing to families seeking value for money. However, commuting from the suburbs to urban job centers can increase transportation costs and time. Lifestyle benefits in suburban areas include quieter neighborhoods and community-oriented living. Weighing these factors, potential homeowners must consider personal priorities, such as space versus convenience, when choosing between urban and suburban living.

Final Words

Understanding the salary needed to buy a home in U.S. cities is essential for potential homebuyers.

By analyzing income requirements, mortgage rates, and property taxes, one can make informed decisions about where to live.

The disparities in home affordability across the U.S. highlight the need for financial planning and strategic saving.

Strategic financial planning, including saving for a down payment and exploring financing options, can ease the home-buying journey.

Whether choosing an urban or suburban setting, the affordability landscape demands careful consideration.

Ultimately, knowing the factors influencing affordability can guide prospective homeowners to find the right balance between salary, lifestyle, and housing costs.