Are you aware that global public pension assets have surpassed $55 trillion, significantly impacting the world economy?

Surprisingly, the seven largest markets alone account for a whopping 91% of these assets, revealing the pivotal role they play in financial stability and growth.

This article delves into the fascinating statistics of public pension assets worldwide, unveiling how they are distributed across countries and managed to bolster economic influence.

By examining these surprising insights, readers gain a deeper understanding of the global pension landscape and the economic trends driving future growth.

How are pension assets transforming global economies?

Discover the details in the full article.

Global Public Pension Assets: An Overview

How much do global pension assets amount to?

Global pension assets across 22 major markets, known as the P22, have reached US$55.7 trillion. This staggering figure highlights the immense scale and economic importance of pension assets worldwide, representing 69% of the GDP of these economies.

Which countries make up the seven largest pension markets?

The seven largest pension markets, collectively referred to as the P7, dominate the global pension landscape. They account for 91% of total pension assets globally, underscoring their pivotal role in the financial ecosystem. These markets include:

- Australia

- Canada

- Japan

- Netherlands

- Switzerland

- United Kingdom

- United States

Why are global public pension assets significant?

The significance of these assets is profound in terms of global GDP and economic influence. They provide financial stability and sustainability for retirees, fund widespread investments, and contribute to economic growth. The sheer size of these assets means they are critical in shaping financial markets and economies.

How is technology impacting pension asset management?

The integration of human and artificial intelligence in asset management is revolutionizing how these funds are managed. AI enhances decision-making processes by analyzing vast datasets for better investment strategies, risk management, and operational efficiencies. This fusion of technology and human expertise ensures that pension funds are managed more effectively and can adapt to rapidly changing market conditions.

Public Pension Assets by Country: Detailed Statistics

How much do public pension assets vary by country?

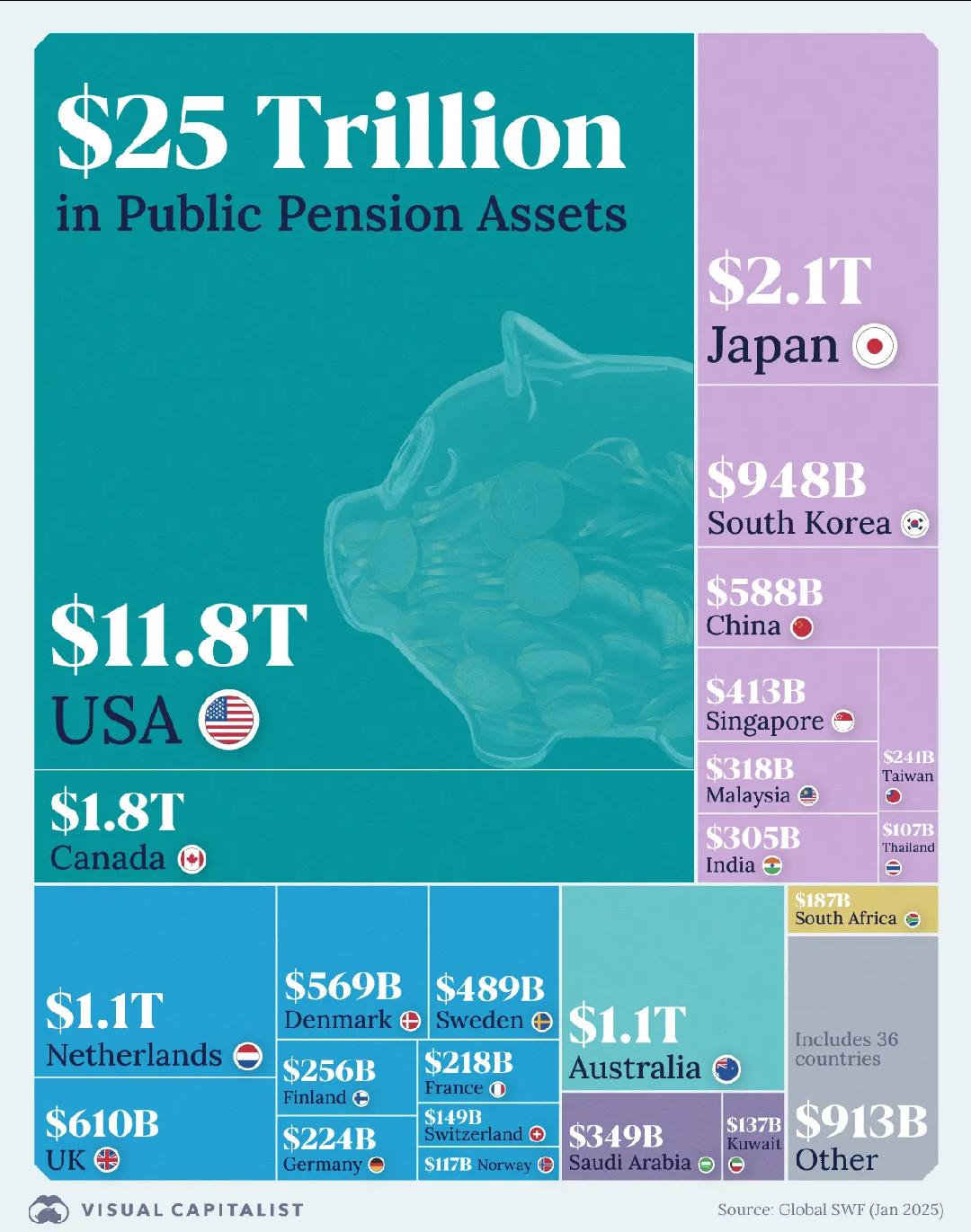

The infographic reveals a total of $25 trillion in public pension assets distributed globally. The United States leads with a significant share of $11.8 trillion, followed by Japan with $2.1 trillion. South Korea holds $948 billion, while Canada, the Netherlands, and Australia each manage $1.8 trillion, $1.1 trillion, and $1.1 trillion, respectively.

| Country | Pension Assets (Trillion USD) |

|---|---|

| United States | 11.8 |

| Japan | 2.1 |

| South Korea | 0.948 |

| Canada | 1.8 |

| Netherlands | 1.1 |

| Australia | 1.1 |

What factors contribute to the differences in pension assets among countries?

The disparity in pension assets is influenced by various factors, including each country's economic size, population demographics, and pension system design. Countries with larger economies, like the United States, naturally have more substantial pension assets. Additionally, nations with aging populations may accumulate more pension assets to ensure long-term sustainability.

Why are these public pension assets significant to each economy?

Public pension assets play a critical role in national economic stability and growth. They provide a safety net for retirees, ensuring financial security and contributing to consumer spending. Moreover, these assets represent significant investment power, influencing both domestic and international financial markets. Countries with robust pension systems can leverage these assets to support economic development and infrastructure projects, thereby enhancing overall economic resilience.

Trends and Growth in Public Pension Assets

What are the current trends in public pension asset growth?

Pension assets are witnessing robust growth, underscoring their increasing importance within the global financial landscape. This growth is driven by several key trends:

- Demographic Shifts: Aging populations in many countries are pushing pension systems to expand, ensuring sufficient funds for retirees.

- Economic Recovery: Post-pandemic economic recovery has bolstered asset values, contributing to increased pension fund sizes.

- Technological Advancements: Adoption of AI and data analytics in asset management is enhancing investment strategies and operational efficiencies.

How do economic factors affect pension asset growth?

Economic uncertainties, such as geopolitical tensions and sluggish economic growth, pose challenges to pension asset growth. Interest rates have peaked in many regions, with potential declines anticipated in 2024. These factors can impact investment returns and require pension funds to adjust their strategies to maintain growth.

What is the impact of shifting pension schemes?

The transition from defined benefit (DB) to defined contribution (DC) schemes is a significant trend reshaping pension systems. This shift is driven by:

- Cost Predictability: DC schemes offer more predictable costs for employers, reducing their financial liabilities.

- Increased Individual Responsibility: Individuals bear more responsibility for their retirement savings, influencing their financial planning and investment choices.

These changes have profound implications for the sustainability and management of pension assets, as they adapt to new economic realities and demographic pressures.

Public Pension Fund Allocation and Investment Strategies

How do public pension funds allocate their assets?

Public pension funds typically allocate assets across a diverse range of classes to balance risk and return. Common asset classes in these portfolios include equities, fixed income, real estate, and alternative investments such as private equity and hedge funds. This diversification helps to mitigate risks and enhance potential returns, ensuring that funds can meet their long-term liabilities.

What role does responsible investment play in pension fund strategies?

Responsible investment practices are crucial for sustaining cash flows required for member benefits. By incorporating environmental, social, and governance (ESG) criteria into investment decisions, pension funds can address potential risks and opportunities that may impact their financial performance. This approach not only aligns with ethical considerations but also seeks to enhance long-term returns by investing in sustainable and resilient businesses.

How are governments influencing pension investment strategies?

Governments are increasingly shaping pension investment strategies by encouraging allocations in domestic economies and higher-risk ventures. This influence often aims to stimulate local economic growth and development. By directing pension funds to invest in infrastructure projects or emerging industries, governments can leverage these significant financial resources to support national economic objectives, while also potentially offering attractive returns for the pension funds.

What is the balance between risk and return in these investment decisions?

Balancing risk and return is a fundamental aspect of pension fund investment strategies. Funds must carefully assess the risk profile of their investments to ensure they can meet their obligations to beneficiaries. This involves strategic asset allocation, regular portfolio reviews, and adjustments in response to changing market conditions and economic forecasts. By maintaining this balance, pension funds strive to achieve stable growth and financial security for their members.

Comparative Analysis of Public Pension Systems

What role do public pension plans play globally?

Public pension plans are essential for providing retirement and disability benefits. They serve as a financial safety net for millions, governed by public sector laws that ensure their operation and sustainability. These systems are a cornerstone of social security in many countries, helping to mitigate poverty among the elderly and disabled by providing consistent income streams.

How are public pension systems governed?

Governance structures of public pension systems vary significantly across countries. Some are centrally managed by government bodies, while others operate through independent agencies. This diversity reflects different national priorities and regulatory environments, impacting the efficiency and effectiveness of pension delivery.

Which are the largest public pension funds in the U.S.?

The U.S. is home to some of the largest public pension funds, including:

- Federal Retirement Thrift Investment Board

- California Public Employees’ Retirement System (CalPERS)

- California State Teachers Retirement System (CalSTRS)

These funds manage vast resources, ensuring the financial stability of millions of American retirees.

What are the differences and similarities in pension system designs?

Public pension systems worldwide share the common goal of providing financial security, yet they differ in design. Some rely on pay-as-you-go models, while others are fully funded. These variations affect the level of benefits and the financial sustainability of the systems. Similarities include the universal aim of protecting retirees, but differences in funding and benefit structures can significantly impact the quality of life for beneficiaries.

Future Projections and Challenges for Public Pension Assets

What is the ongoing trend in pension schemes?

The shift from defined benefit (DB) to defined contribution (DC) pension schemes is an ongoing trend. This transition is primarily driven by the need for cost predictability for employers and increased life expectancy. In DC schemes, individuals bear more responsibility for their retirement savings, altering the landscape of pension fund management and sustainability.

What challenges do demographic changes pose to pension systems?

Increased life expectancy poses significant challenges to pension systems. As people live longer, pension funds must ensure they have enough assets to cover longer retirement periods. This demographic shift demands more robust financial planning and may increase pressure on pension systems to deliver sustainable benefits over extended durations.

What are the potential risks for pension fund sustainability?

Pension sponsors rely on achieving asset portfolio targets, which often depend on continuous bull markets. If these targets are not met, taxpayer liabilities may increase, posing a risk to pension fund sustainability. Economic volatility and market downturns can exacerbate these risks, making it crucial for pension funds to adopt strategies that mitigate potential financial shortfalls.

What strategies can ensure long-term sustainability?

To ensure long-term sustainability, pension funds are exploring diversified investment strategies, incorporating both traditional and alternative asset classes. Emphasizing responsible investment practices and leveraging technology for better risk management are also key strategies. These approaches aim to secure stable returns and manage the financial obligations of pension systems effectively.

Final Words

Global public pension assets demonstrate the massive scale and reach of these financial vehicles.

With US$55.7 trillion across major markets, these funds are pivotal, accounting for 69% of GDP in key economies.

Countries like the USA, Japan, and Canada lead in pension asset accumulation, showcasing vital economic roles.

Pension assets are not static; they are growing amid global challenges.

With a growing emphasis on responsible investment, public pension funds navigate the balance of risk and return.

The comparative analysis of various systems highlights differing structures and strategies.

Moving forward, the transition from defined benefit to defined contribution schemes signals evolving sustainability needs.

Despite challenges such as demographic shifts, the continuous adaptation and forward-thinking strategies ensure these funds remain robust.

Understanding public pension assets worldwide statistics is crucial for safeguarding financial well-being in diverse economies.